June 2023 East Bay Market Report

Market Update

Market Update

Note: You can find the charts & graphs for the Big Story at the end of the following section.

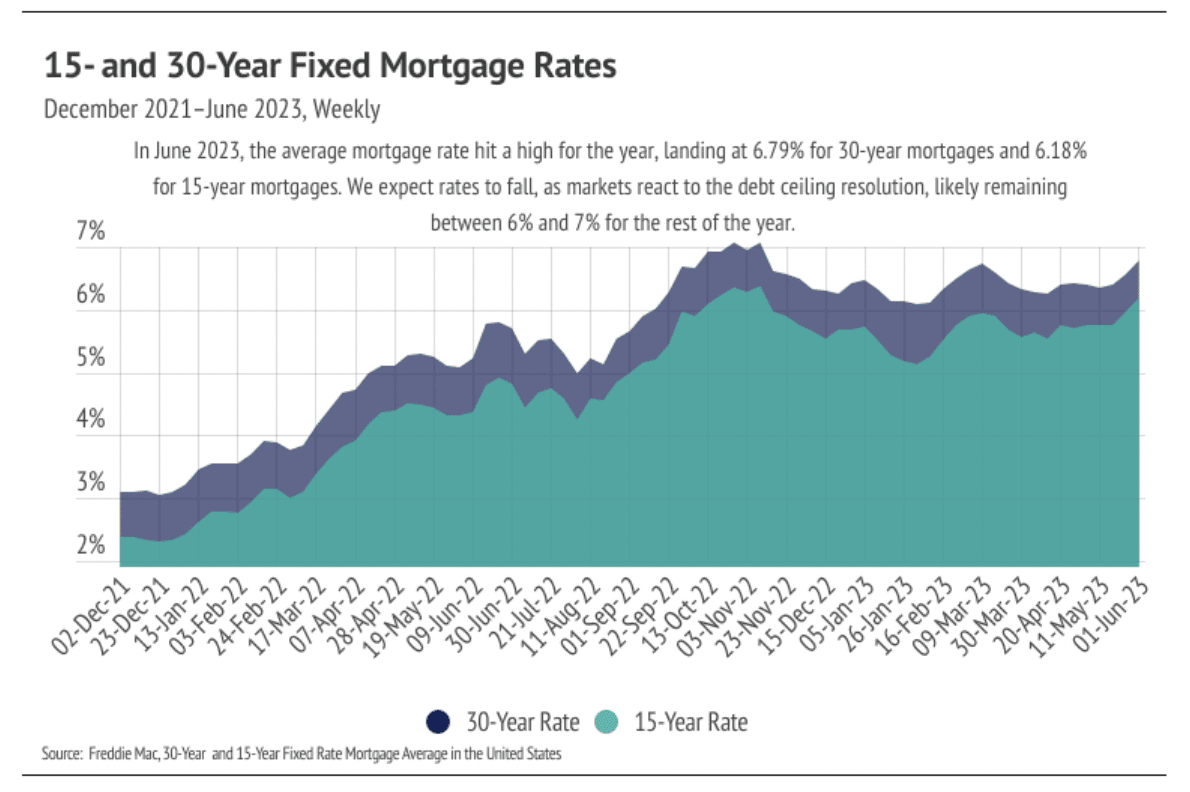

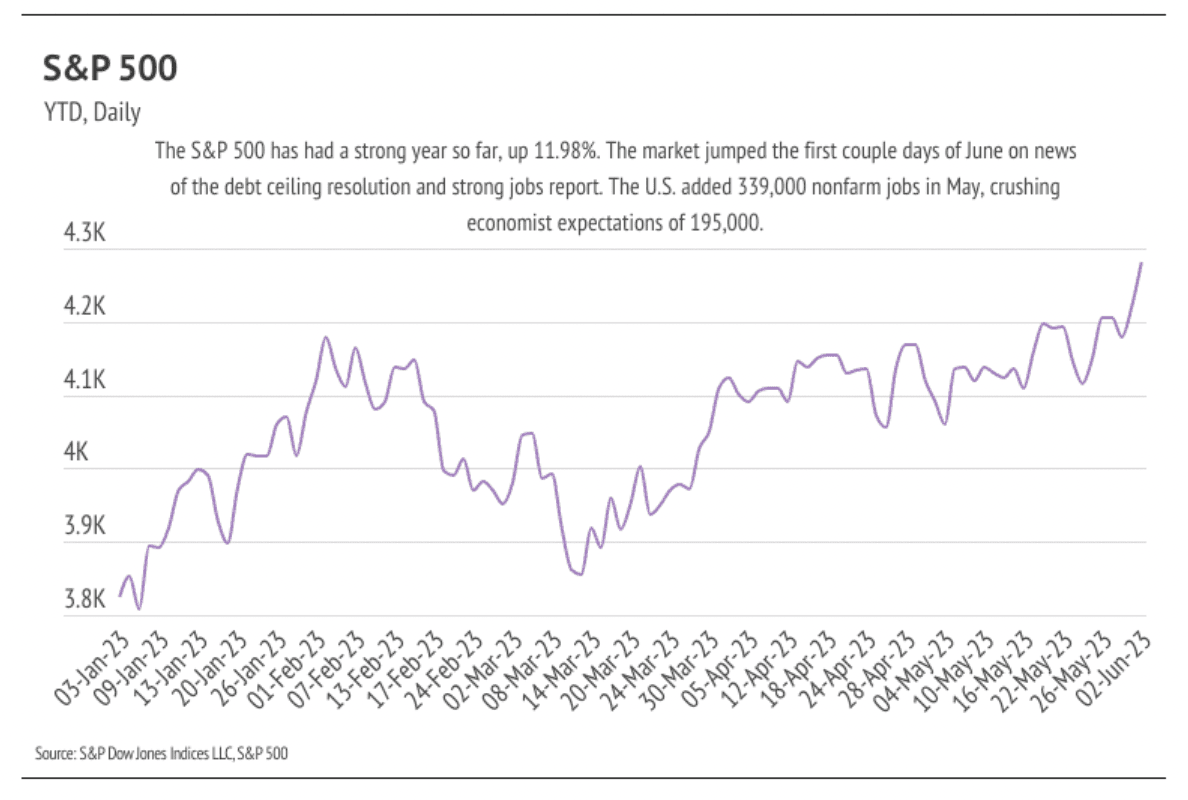

Great news! We've successfully navigated yet another debt ceiling crisis, showing once again the resilience of the United States. We paid our bills in full and on time, preventing a disastrous default and sparing the world from an economic catastrophe. The repercussions of a default would have been felt far and wide, including the unwelcome consequence of significantly higher mortgage rates. Despite concerns about this Congress being more inclined towards default, the financial markets remained remarkably unfazed. In May, the 10-year Treasury yield experienced a modest uptick of 0.4%, leading to a corresponding 0.4% increase in the average 30-year mortgage rate. On a positive note, the S&P 500, which tracks the stock performance of the largest publicly traded U.S. companies, reached its highest point of the year at the beginning of June, showing an impressive year-to-date growth of 12%.

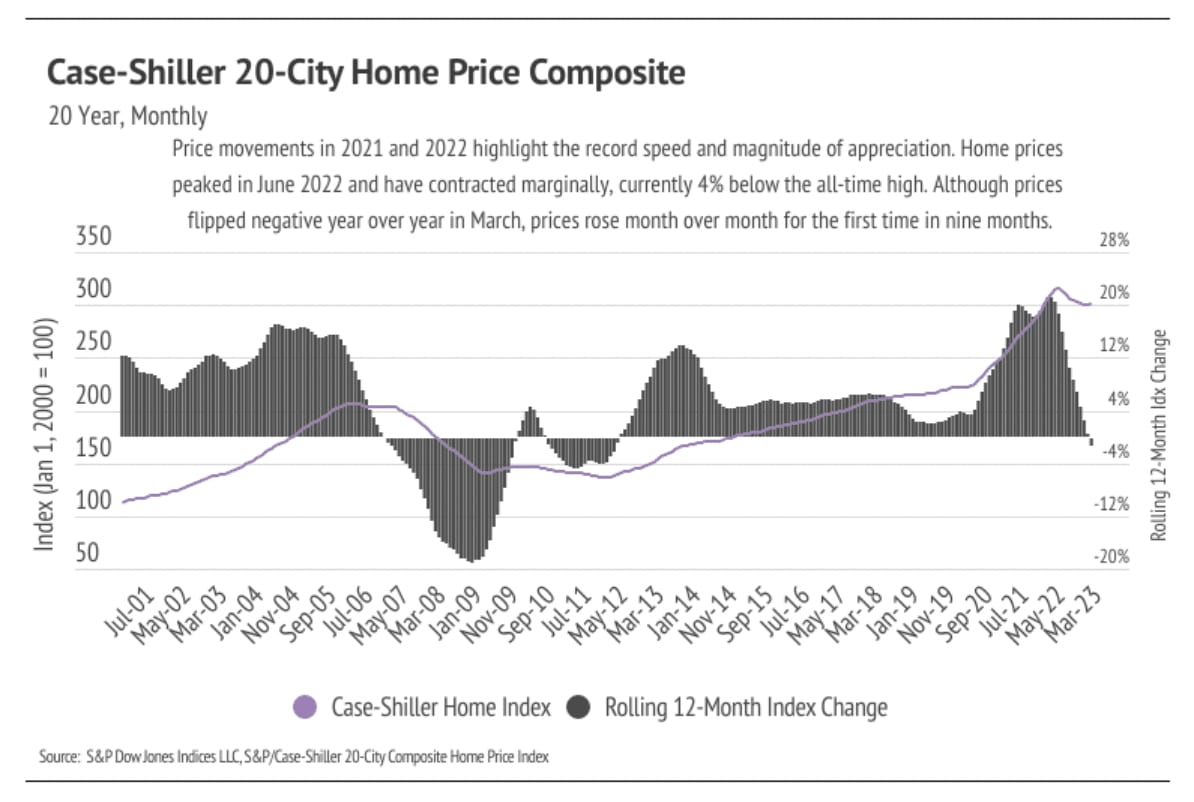

Now that we have temporarily lifted the debt ceiling until 2025, our attention shifts back to the Federal Reserve and its decisions regarding interest rates. During their latest meeting, the Fed indicated a potential pause in rate hikes after three significant regional bank failures this year. However, recent job data may sway them towards a 0.25% increase. Rising mortgage rates have largely driven the housing market slowdown we've witnessed over the past year. Fluctuations in rates have presented challenges for potential homebuyers, as the average 30-year mortgage rate went from historic lows in 2021 to a 20-year high in November 2022. Fortunately, rates have come down since then, hovering around 6.5%. Given that home prices haven't experienced substantial declines from their peak levels, even small rate changes can significantly impact financing costs. Although the average 30-year rate reached a 2023 high in June, we anticipate rates to remain within the 6-7% range this year. It's important to note that the Fed tends to make gradual adjustments to rates over time, so each increase will likely be followed by a decrease, prolonging the process of returning to lower mortgage rates.

The Fed faces a challenging decision regarding future rate hikes. On one hand, the labor market has shown impressive strength and appears resilient to rate increases. Monthly employment figures consistently surpassed expectations, with May alone seeing the creation of 339,000 jobs, surpassing the anticipated 195,000. On the other hand, unemployment experienced a slight uptick from April to May. Additionally, the first-quarter 2023 GDP data was revised upwards, indicating a quarter-over-quarter growth of 1.3%. With this mixed set of data, we expect a pause in rate hikes at the June meeting, followed by a potential hike in July.

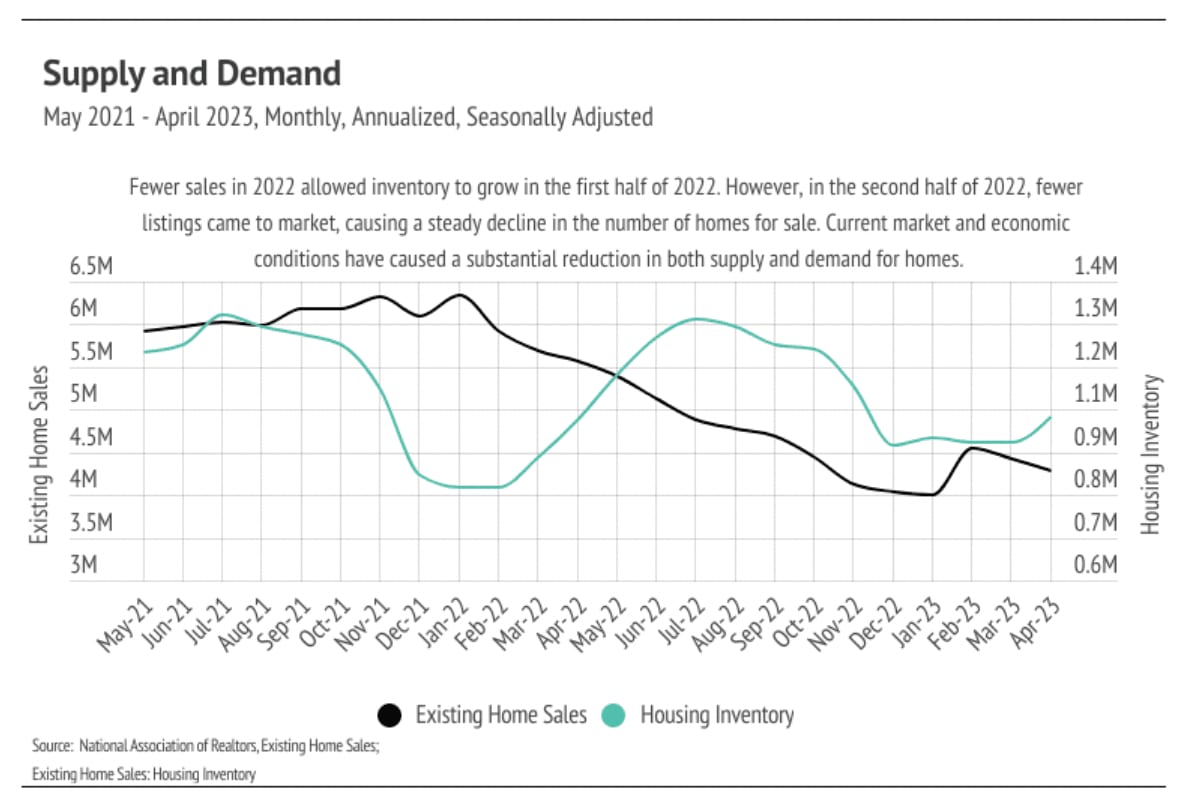

The housing market finds itself in an intriguing position, where the economy's overall strength makes lowering rates unlikely, but home prices have become increasingly unaffordable for potential buyers. The market is experiencing fewer sellers and buyers, so meaningful sales growth is not expected this year.

It's important to note that regional and individual housing markets may deviate from national trends. We've included a Local Lowdown section to provide you with detailed coverage for your specific area. As a general observation, higher-priced regions like the West and Northeast have been more affected by mortgage rate hikes compared to more affordable markets in the South and Midwest, considering the absolute dollar cost of rate increases and limited opportunities for new home construction. Rest assured, we'll continue to closely monitor both the housing and economic markets, providing you with the best guidance for buying or selling your home.

Note: You can find the charts/graphs for the Local Lowdown at the end of this section.

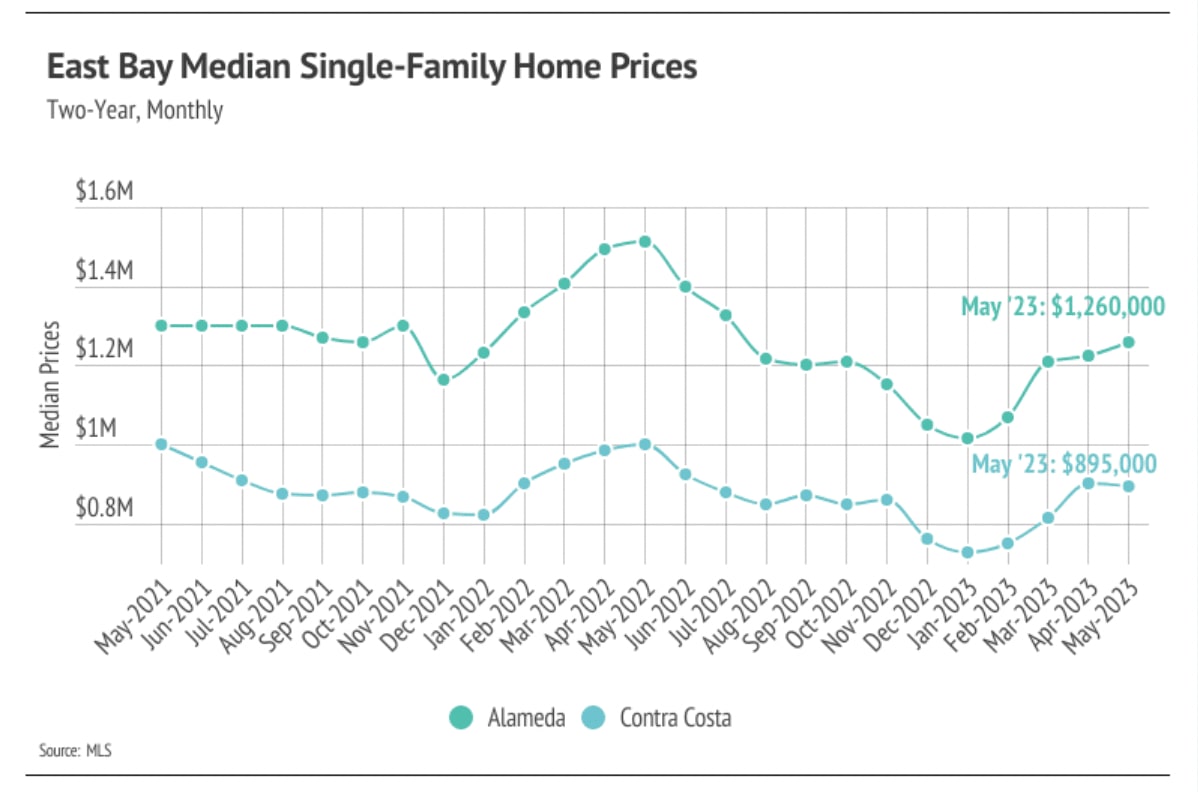

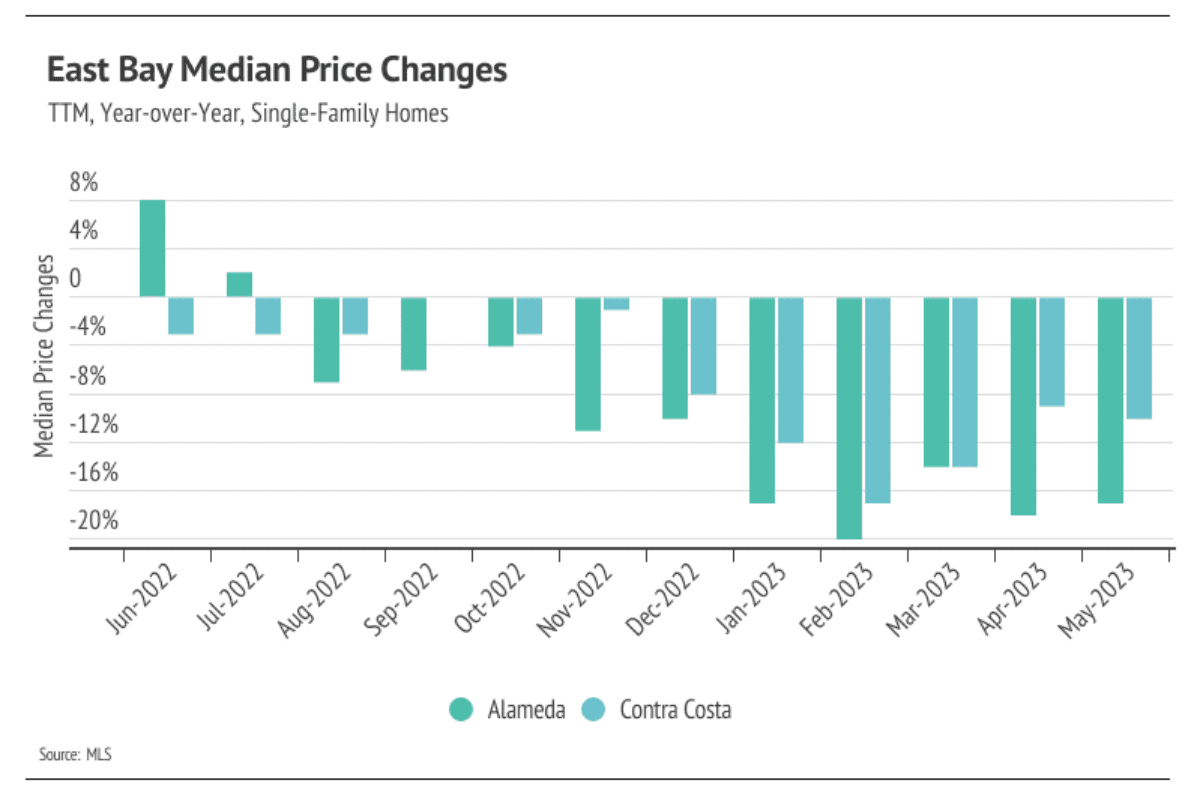

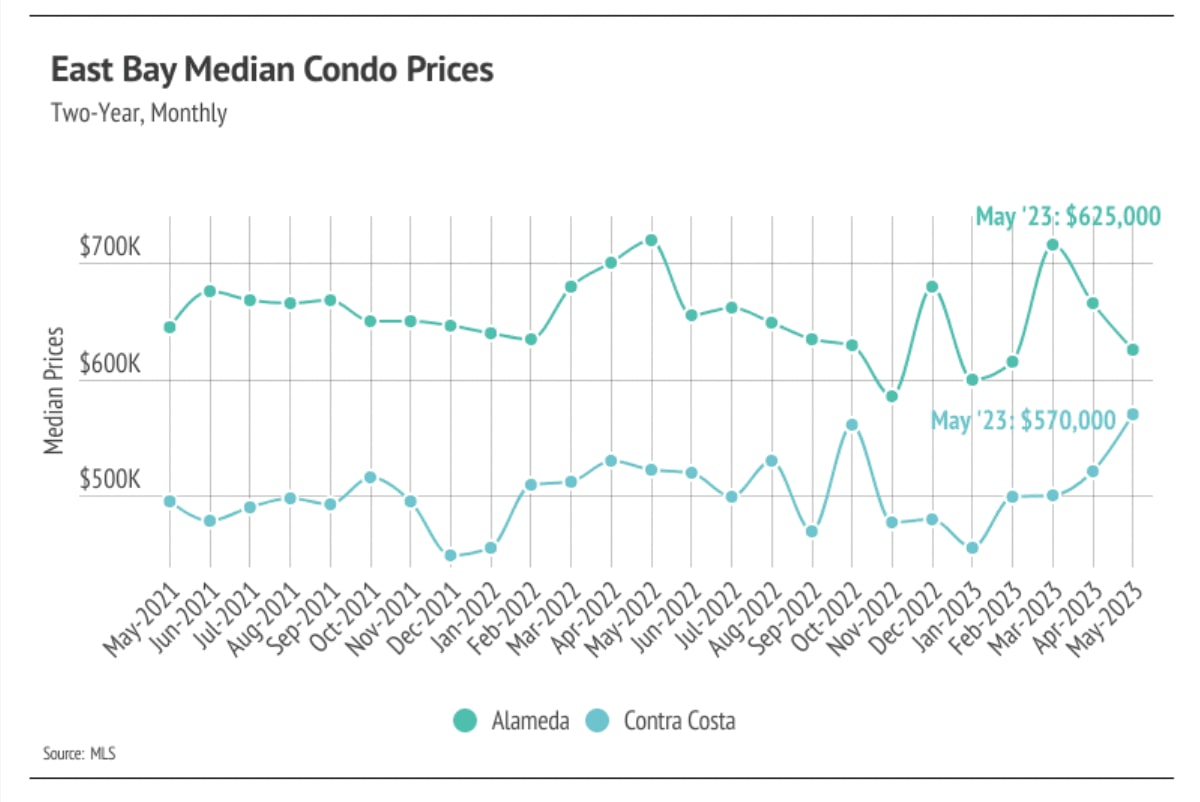

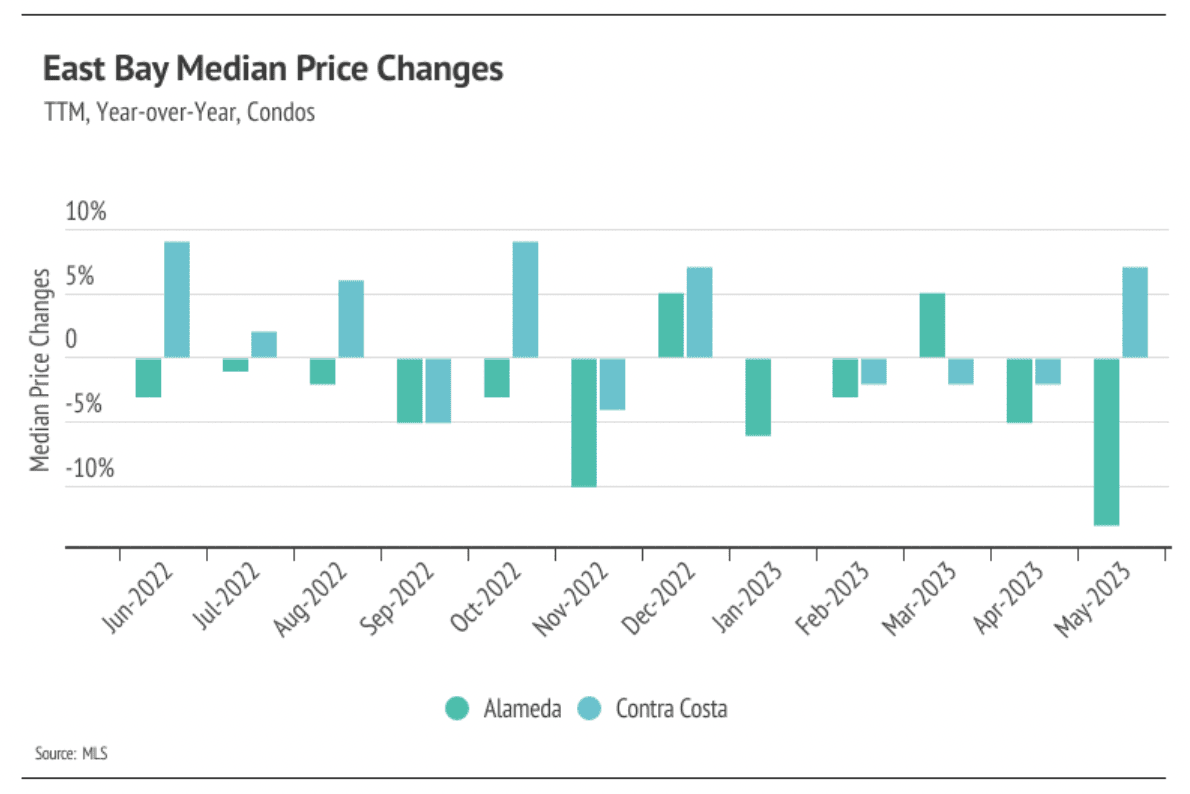

The East Bay has seen remarkable price appreciation this year, with significant gains across the board. Single-family home prices in Alameda surged by an impressive 20%, while Contra Costa experienced a substantial 17% increase. Condo prices in Contra Costa even reached an all-time high in May. This surge in home prices can be attributed to the combination of increasing demand and a gradually rising inventory.

In the previous year, homebuyers rushed to secure lower mortgage rates as the Fed announced rate hikes at the end of 2021 that would impact rates in 2022. The average 30-year mortgage rate climbed by 2% in the first four months of 2022, surpassing 5% for the first time since 2011. This significant jump in rates resulted in a 27% increase in the monthly cost of financing, prompting buyers to enter the market swiftly. As rates continued to rise, the market naturally cooled, leading to a decline in home prices as buyers adjusted to the higher costs associated with mortgages. Consequently, both supply and demand were lower than usual in the latter half of 2022.

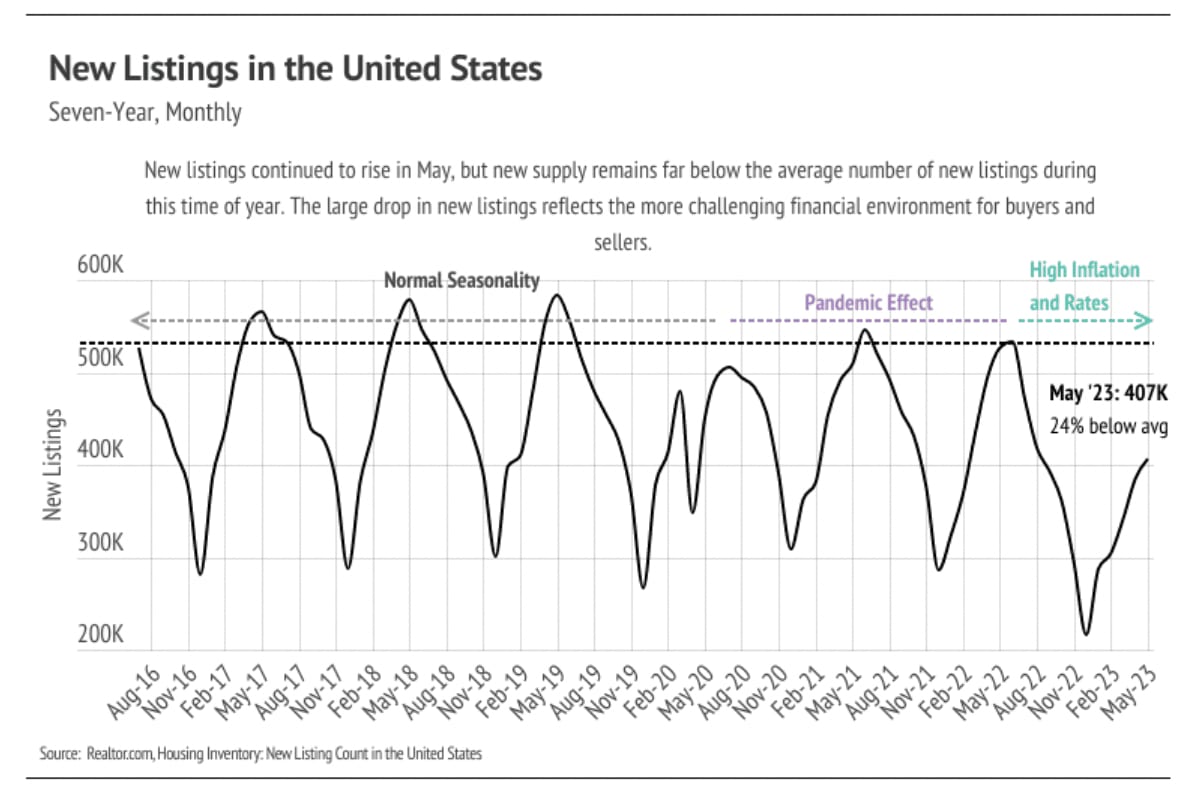

However, in 2023, we witnessed a resurgence in demand, even with elevated mortgage rates, accompanied by a notable increase in new listings. The price increases we have observed this year are largely attributed to the growth in inventory and the greater availability of homes on the market, which is counterintuitive to the conventional dynamics of supply and demand. With the limited supply of homes, more properties were able to align with buyers' preferences, providing sellers with increased pricing power. As we move into the summer months, we anticipate a further rise in demand, leading to heightened competition among buyers and consequently driving home prices even higher.

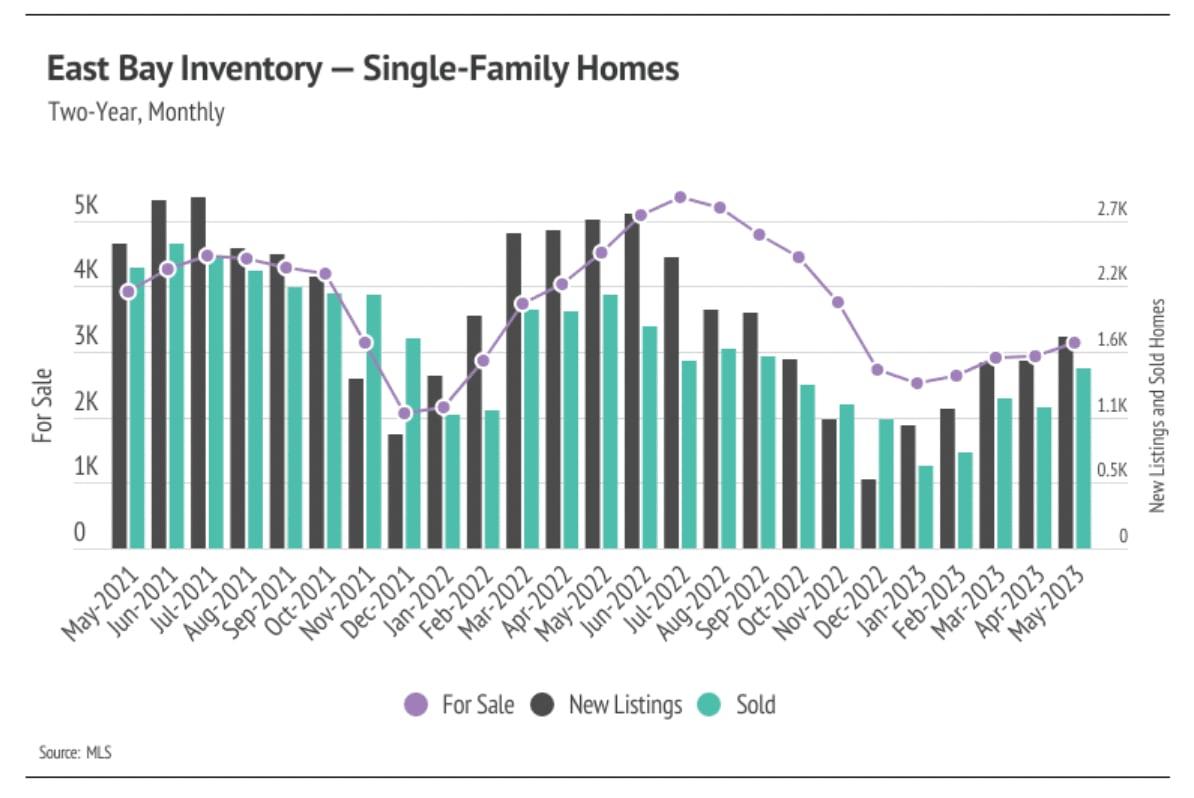

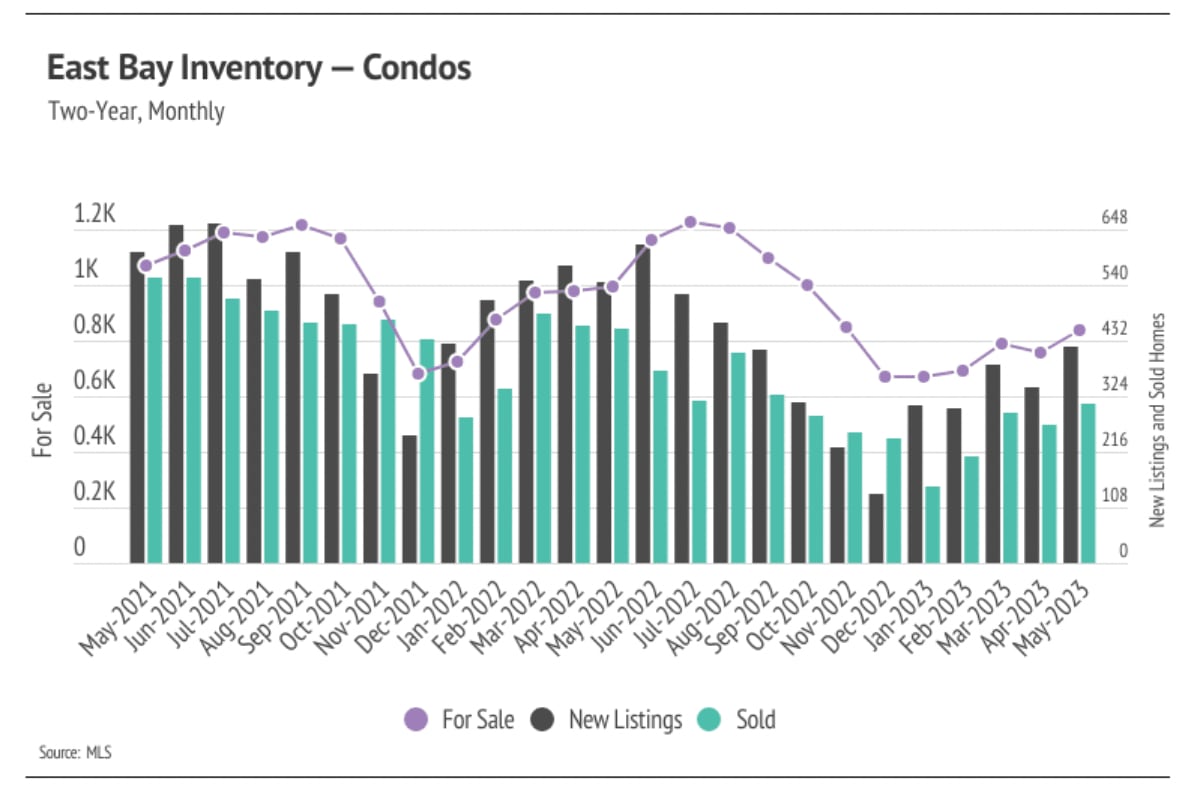

Over the past four months, we've seen positive developments in the East Bay's housing market, with increases in single-family home and condo inventory, sales, and new listings. While it's important to note that these metrics still remain below their usual levels, these upward trends indicate a healthier market overall. Despite the current inventory being lower than the demand, there is room for more new listings to enter the market. Homeowners who have fully paid off their properties find themselves in a particularly advantageous position, especially if they don't require financing for their next home after selling their current one. Since January, we've observed an impressive 116% increase in sales and a 63% rise in new listings.

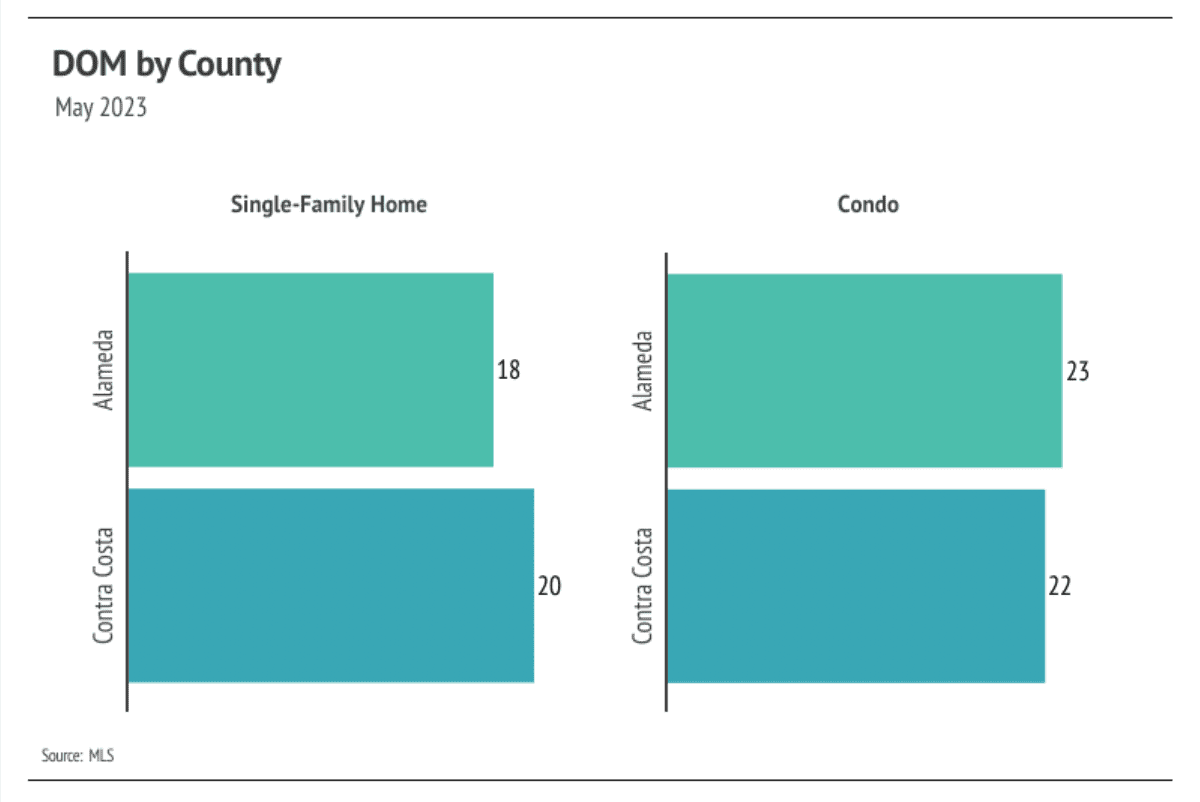

As buyer competition intensifies and sellers gain more negotiating power, we're seeing sellers receive a greater percentage of their listed price. In January 2023, sellers received 95% of their list price, whereas, in May, that number rose to 104%. Looking ahead, inventory will likely remain limited throughout the rest of the year, setting the stage for a market that will only become more competitive, particularly during the summer months.

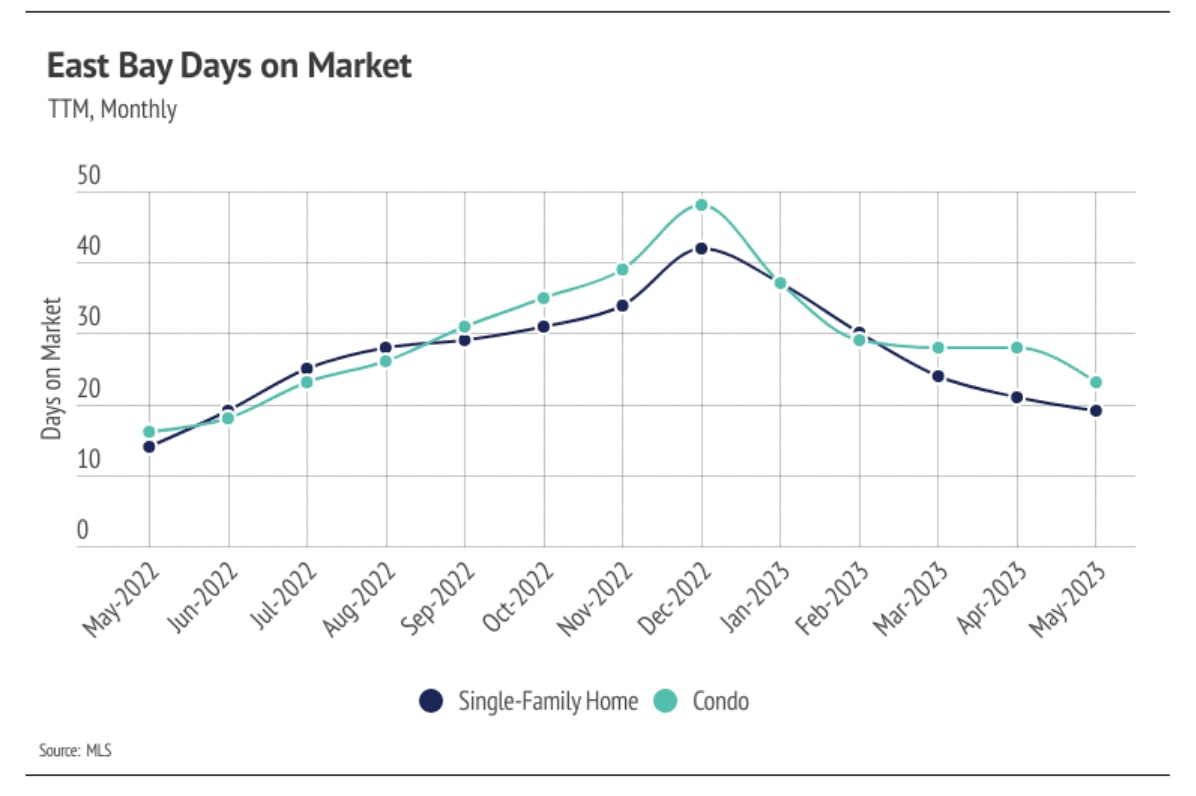

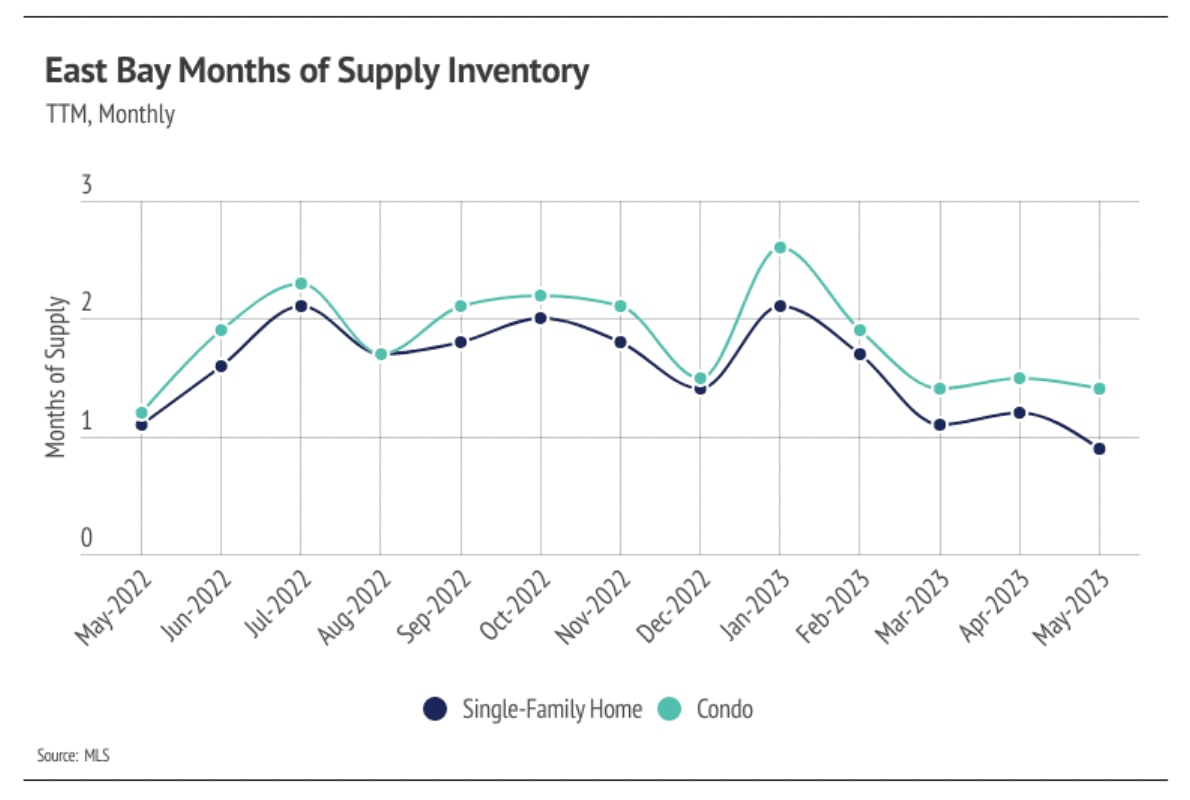

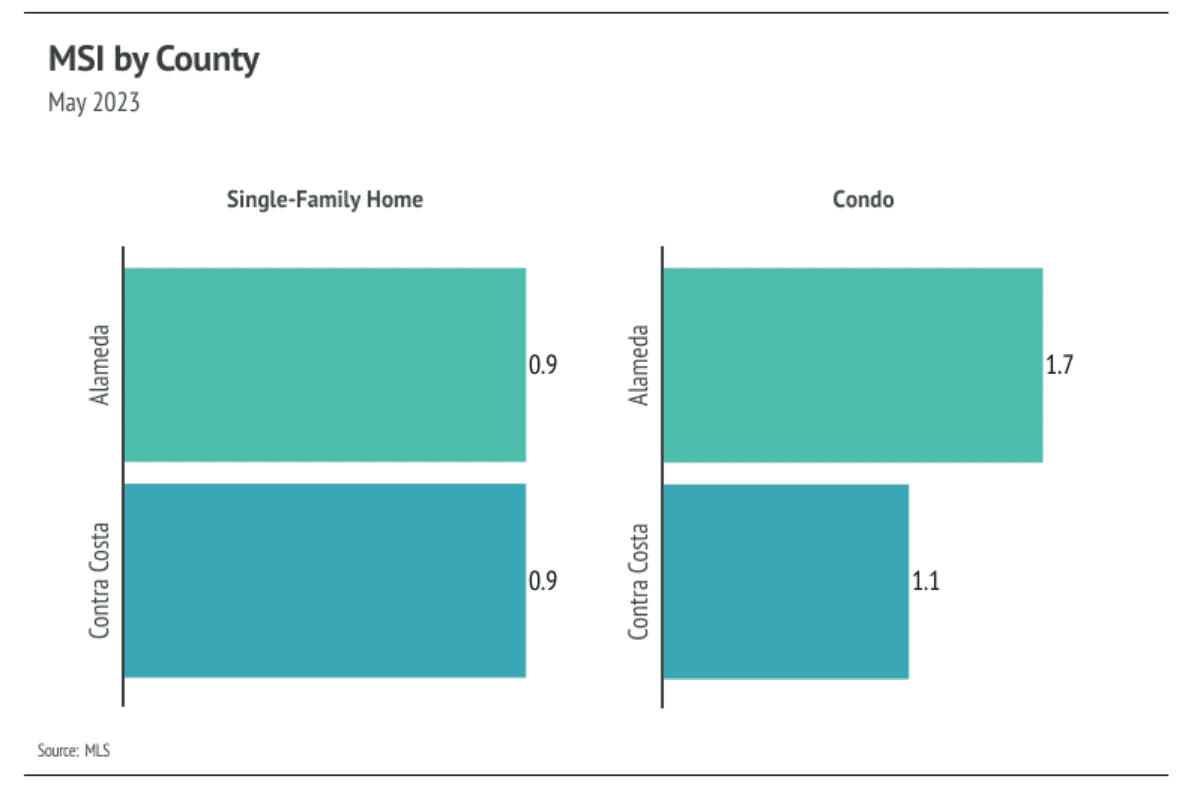

When analyzing the housing market, one crucial indicator that helps us understand the supply and demand dynamics is the Months of Supply Inventory (MSI). It provides valuable insights by measuring the number of months it would take for all the currently listed homes to sell at the current rate of sales. In California, the long-term average MSI hovers around three months, which typically indicates a balanced market.

In the East Bay, however, the market tends to lean in favor of sellers, particularly for single-family homes, as evidenced by its lower MSI. An MSI below three signifies a sellers' market, suggesting that there are more buyers than available properties. On the other hand, a higher MSI indicates a buyers' market with an abundance of homes relative to the number of prospective buyers.

Over the past four months, we've observed a further decline in the MSI for both single-family homes and condos in the East Bay, indicating an even stronger advantage for sellers. This drop can be attributed to a higher proportion of sales compared to active listings and reduced time spent on the market for properties. These factors have contributed to a market environment where sellers hold more leverage and enjoy increased buyer interest.

Rest assured, we will continue to closely monitor the MSI and other key indicators to provide you with up-to-date insights into the East Bay's real estate landscape. Whether you're looking to sell or buy a property, we are here to guide you through the intricacies of the market and ensure your journey is smooth and successful.

Stay up to date on the latest real estate trends.

Market Update

Agent of the Month

Market Update

Real Estate

Real Estate

Market Update

Real Estate

Market Update

Real Estate

You’ve got questions and we can’t wait to answer them.